Consumer proposals offer a solution for managing debt. They mainly focus on unsecured loans like credit cards, medical bills, personal loans, and student loans.

Proposals let debt owners combine their unsecured loans into a single payment. Debtors can make this payment either in full or through monthly installments.

This debt management strategy has seen an increase in recent years. What led to this rise were the changes made to the Bankruptcy and Insolvency Act (BIA) in 2009. It was at that time, the maximum debt limit for a consumer proposal was raised from $75,000 to $250,000. This meant many more Canadian debt holders were eligible to do a consumer proposal, whereas previously Bankruptcy would have been their only option. Changes also stipulated that financial counselling be mandatory for proposal recipients.

While the updated BIA certainly had a hand in the increase in consumer proposals, it’s important to acknowledge that other social factors also played a role in this increase. At that time, inflation was a hot topic and credit cards were rapidly gaining popularity.

Consumer proposal timeline

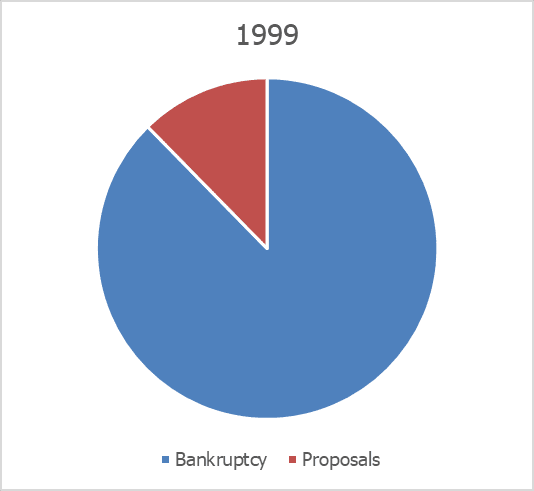

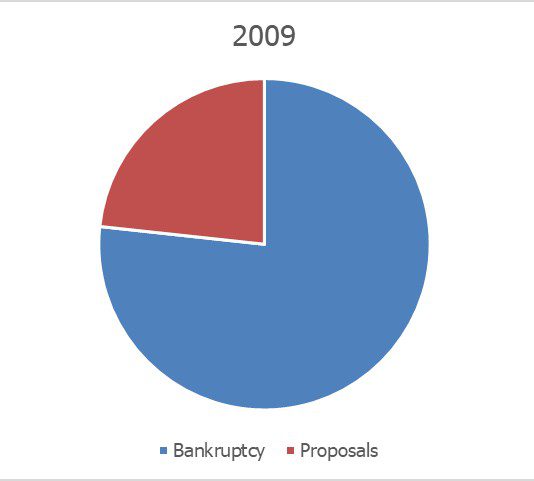

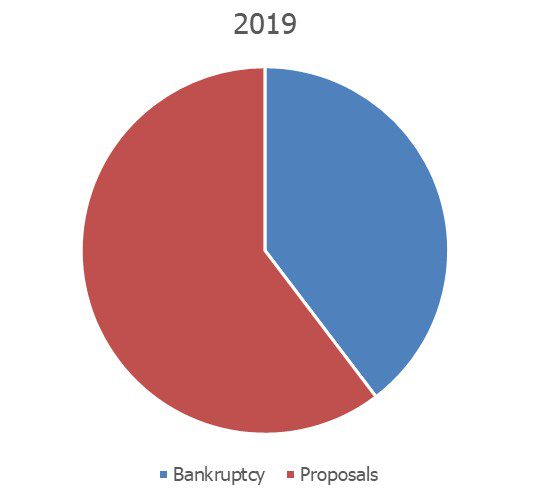

The pie charts below show changes between Bankruptcy and Consumer Proposal trends from 1999 to 2019. It demonstrates how drastically more popular Consumer Proposals became after the 2009 changes came into effect. In fact, the volume of consumer proposals rose by about 134.3% from 2009 to 2019 alone.

Proposals and increase in debt obligations

As inflation increases in Canada, so does the number of consumer proposals. We’re in a perfect example of that right now. While inflation has now slowed, Canadians are struggling to recover from its not-so-long-ago 8.1% wallet-squeezing high. Canadians needed, and still need, help paying for essential items like food and shelter. To compensate for the rise in costs, some people use credit cards or take out personal loans just to survive.

Using credit cards leads to an increase in high-interest debt. High-interest debt has the potential to quickly become unmanageable. Some people see a consumer proposal as a way, the only way for some, to get back on their feet financially. Just this past year is a great example. When comparing the number if consumer proposals between first quarter of 2023 vs 2024 there was an increase of over 15%. Meanwhile, bankruptcies only went up a little over 9%.

Looking back to 2009 when the changes were implemented to the BIA, on average, Canadians had $20,200 in non-mortgage debt. In 2019, that number jumped to $36,900. That’s an increase of 82%. A lot more people were relying on debt and a lot more debt. These debt loads definitely played a role in the rise of consumer proposals.

Canadians saw proposals as an alternative to bankruptcy

During the 2008 to 2009 global recession, many Canadians felt the woes of financial pressure. Many were weary of the idea of Bankruptcy but saw consumer proposals as an attractive alternative now that they were eligible. Below are some of the other advantages of doing a Consumer Proposal compared to other debt solutions.

Asset Protection

Consumer proposals have become more popular because they let debt owners keep most of their assets.

The items that debtors can hold on to depend on the province that they live in. Some items, like clothing, food and RRSPs are exempt across Canada. Other items are only exempt in certain provinces. Further to that, the allowable number or value of some nationally exempt items varies across provinces. For example, in New Brunswick, debtors may keep their vehicle if it’s worth $6,500 or less. In Ontario, vehicles valued at $6,600 or less are exempt.

Family Sponsorship

The ability to continue to sponsor family members from overseas added to the appeal of consumer proposals. This debt relief solution makes it easier for new Canadians to keep sponsoring their family members to come to Canada without any issues. However, if a debt owner files for bankruptcy, their request to sponsor will be declined.

Security

The demand for proposals has also risen because of the legal shield they provide. When a Licensed Insolvency Trustee (LIT) arranges a payment plan that debt collectors accept, they must stop contacting the person who owes them money. Also, the debt collection agencies can’t take any legal action against them.

Optimism

Hope is another component adding to the boost in proposals.

CBC News recently interviewed Zaki Alam. He is a LIT, and he explained why Albertans have an optimistic view of proposals.

“[Albertans are] saying, well, I can make a payment to my creditors over five years. [In] the next few years, I will get a better-paying job. [I will] get a second job, or things will get better in our economy. And then I can pay off the proposal sooner, and it’ll be off my credit rating sooner,” Alam said.

Proposals have downsides

Even though proposals are an effective debt relief solution, they do have several drawbacks.

- Proposals can damage credit ratings

- Creditors may decline a proposal

- Proposals can take longer to complete than other debt solutions.

- Debtors who have too many assets may be unfit for a proposal

- If a proposal is rejected, creditors may undertake whatever actions they consider essential to retrieve their funds.

- If a debtor misses three ensuing payments, the proposal can be considered void.

- If a debtor doesn’t go to the mandatory financial management courses, the proposal may be considered void.

Final thoughts

The updated 2009 BIA made proposals more popular in Canada. In the simplest of terms, the changes made it a viable option for more people. Especially the increase in the debt loads eligible. It’s also a more attractive option because, among other things, there’s less chance of losing assets and a lower impact on credit.

This debt relief solution gives borrowers hope of regaining control of their finances. Learn more about consumer proposals or other debt solutions by contacting one of our expert Credit Counsellors.