Understanding Bankruptcy

Reviewed by:

What happens when you need to declare bankruptcy in Canada?

The reasons for declaring bankruptcy in Canada vary by household. Job loss, divorce, cost of living, high interest rates, and simply not following a budget can all lead to bankruptcy. Bad things can happen to good people, and events during the past few years have certainly been challenging.

There was a sharp drop in filings for bankruptcy during the height of the pandemic. Since then, while still rising, the numbers seem to have levelled out. According to the Office of the Superintendent of Bankruptcy (OSB), total consumer bankruptcies increased by 4.3% in 2025, compared to a 10.8% YoY increase in 2024. Higher interest rates and the rising cost of living over the past few years have played a role in this trend.

Financial hardship can happen to anyone. Even responsible people may find themselves overwhelmed by debt due to circumstances beyond their control. This guide can help you understand how bankruptcy works in Canada, what you can expect when you file, and what will happen once your filing is complete. In this guide, we’ll focus on personal bankruptcy; however, there are other types of bankruptcies for small businesses and corporations.

What is bankruptcy?

Bankruptcy is the legal process by which you are declared insolvent, meaning you owe more than your assets are worth. The process is overseen by a Licensed Insolvency Trustee (LIT). They oversee the sale of any assets that you have that do not qualify for exemption in the province or territory where you live. The proceeds of those sales are used to repay your creditors, and then the remaining balances on the debts included in your bankruptcy are discharged.

How to file for bankruptcy

Step 1: Contact a Licensed Insolvency Trustee (LIT)

You are required to work with a Licensed Insolvency Trustee (LIT) who will help you file your bankruptcy paperwork, oversee the terms of your bankruptcy, and work with creditors on your behalf. The government provides a helpful tool to find an LIT in your area.

You should look them up online before choosing one to see if there are any positive or negative reviews about them. You can find reviews on sites such as Google, Reddit, Trust PIlot, and the Better Business Bureau.

Step 2: Gather your paperwork

When you meet with your Licensed Insolvency Trustee, they will go through your finances with you to determine if you are insolvent.

To do this, you will need copies of personal documents, including tax forms, pay stubs, proof of income, and expenses. They may need more depending on your financial situation, employment, and assets.

Step 3: Meet with your trustee

This will occur at your trustee’s office. The trustee will explain all options available to you. They will ask about your income, your assets, how much you owe, and what your expenses are. They will likely first examine if there are debt relief options and strategies available to you other than bankruptcy.

You should also ask questions, including how to start, what the costs are, when to make payments, what assets you may have that would qualify for exemption, and any other questions you have.

At the end of the meeting, if bankruptcy is the appropriate option and you want to go ahead, the process will begin, starting with you filling out an application.

The information that you will need to disclose is your personal information (full name, address, DOB, etc.), any assets that you have, and a list of your creditors.

Step 4: File for bankruptcy

At this stage, the trustee will file the bankruptcy application and all the necessary paperwork on your behalf with the Office of the Superintendent of Bankruptcy Canada.

Once it is filed, the trustee will begin overseeing the legal obligations for your bankruptcy. You will stop making payments, and any legal action against you, including wage garnishment, will end. They will also contact your creditors. After you’ve filed for bankruptcy, your creditors are prohibited from contacting you or garnishing wages.

Unless a meeting of creditors is requested, you will skip to Step 6.

Step 5: Meet with your creditors (possibly)

In some cases, you may be required to attend a meeting with your creditors. This happens if creditors object to your filing. It only occurs if a minimum of 25% (dollar-based) of your creditors ask for this meeting. The location will usually be your trustee’s office. Before the meeting, you will have to have a preliminary report filled out, which goes over your assets and liabilities, as well as why the bankruptcy happened. It will include details of any business or personal transactions you might have, or will have, been involved in. Your trustee will be present to make sure the process is fair. You can get a lawyer if you wish, but it’s not required.

If a majority of your creditors (dollar-based) agree, your bankruptcy will proceed.

A note on asset sales

When you file for bankruptcy, it isn’t uncommon that you will be required to sell some of your assets in order to pay creditors. Some assets are exempt from this process, but it varies from province to province. For example, in some cases, you will be required to repay any equity that you’ve built up in your home. You could be looking at withdrawing RRSP contributions, selling cars and other property, and more.

Step 5: Take care of your responsibilities

Once you file for bankruptcy officially, you must:

- Attend two counselling sessions to help you develop a good financial management strategy as you move forward.

- File regular reports on your income and expenses,

- Pay costs, including: equity in assets, surplus income, administrative fees, and taxes, which your LIT files.

As part of your bankruptcy agreement, you will be required to pay your LIT a fee for their services in overseeing your bankruptcy process. Additionally, you may be required to make surplus income payments. Surplus income payments are made when your income is above the income threshold amount set out by the Office of the Superintendent of Bankruptcy. A percentage of any income earned above that threshold is required to be handed over to the LIT to be distributed to the creditors.

After nine months, assuming this is your first bankruptcy and you don’t have surplus income, you will be eligible for discharge. This means you no longer owe anything to the creditors listed on your bankruptcy. If you’ve got a lot of surplus income payments to make, or if this is a repeat bankruptcy, you can expect that timeline to take longer.

A note on accepting pay raises during bankruptcy

During your bankruptcy, you must submit reports on your income and expenses. Accepting a raise could bump you over the current standard for your household, which would mean you may have to make surplus income payments. While this may not be ideal, it’s in your interest to accept any increase in pay, even though some of the new funds may go to pay your creditors. Only 50% of your new additional earnings can go towards payments to creditors. The other 50% is yours to keep, income and other taxes notwithstanding. You’ll want to keep that for savings or investments.

Types of Bankruptcy Discharge

- Absolute Discharge – The person in bankruptcy no longer owes any of the debt filed in the bankruptcy form

- Conditional Discharge – The person in bankruptcy must pay additional money over a defined period. When that ends, they may grant an absolute discharge.

- Suspended Discharge – The person in bankruptcy will experience a delay in the absolute discharge date.

- Refused Discharge – The person in bankruptcy does not get a discharge because of a court action.

When you are discharged, your debts are essentially “cancelled.” However, there will be a note on your credit report denoting your bankruptcy, which will stay in place for several years. This can impair your ability to take out credit for an extended period.

The long-term impact on your financial future means that you need to seriously consider the implications before you file for bankruptcy.

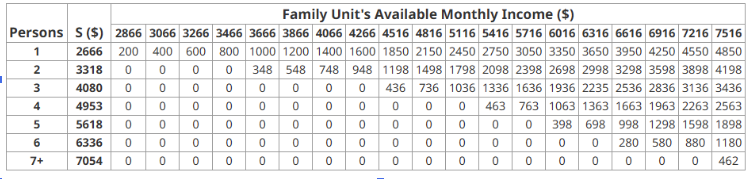

Understanding surplus income in bankruptcy

Surplus income is any income you make over the amount that the Canadian Government claims an individual or family needs to live. According to the Office of the Superintendent of Bankruptcy Canada (OSB), the current income standards in 2025 are:

- $2,666 for a single-person household

- $7,054 for a seven-person or more household

- $3,318 for a two-person household

- $4,080 for a three-person household

- $4,953 for a four-person household

- $5,618 for a five-person household

- $6,336 for a six-person household

Superintendent’s Standards – 2025

Pros and cons of bankruptcy

Advantages:

- No more wage garnishments

- No collection calls or harassment

- No more student loans more than seven years old

- The process can be finished in as little as nine month

Disadvantages:

- No access to credit cards

- You may owe money on the equity of your assets

- The cost (of the process) is higher than some other debt relief methods

- Monthly reporting requirements

- Bankruptcy will be a permanent public record

Rebuilding your credit and finances after bankruptcy

When the process of bankruptcy is over, your LIT will give you a “Notice of Discharge.” This notice means you no longer have those debts. You are debt-free at this point, minus any other obligations that were not part of the bankruptcy. That may include secured debts on assets that qualified for exemption, taxes, child support, alimony, and student loans less than seven years old.

What happens after bankruptcy?

Bankruptcy has a severe effect on your credit. The bankruptcy will stay on your credit report for six years. You will have to build up your credit from scratch. There are a few things you can do to get back on track. If the cause was overspending or living beyond your means, you will want to learn how to make and stick to a budget. Pay attention when your credit counsellor is discussing budgeting with you. If you’ve been through these sessions, you’ve hopefully learned money management skills and know how to keep your budget.

You’ll also need to start paying bills on time; autopay can help with this. Easy ways to start new credit include secured credit cards and other new credit programs. A secured credit card is when you have an account with a credit card company that is secured by a cash deposit. Your credit limit is equal to the amount you deposit. Always follow and keep your budget. Understand what expenses you have and plan for your wants and needs.

Before you decide to file, talk to a trained credit counsellor

Bankruptcy is a tough, life-changing decision to make. You deserve to understand all your available options before making this difficult choice. Talk to a trained credit counsellor for free to discover if a less drastic debt relief choice can work for you so you can avoid bankruptcy.

Frequently Asked Questions

To file for bankruptcy in Canada, you must be a legal citizen, a permanent resident, or someone who lives outside of the country but owns property here. You need to owe more than $1,000. You also need to be “insolvent,” which means that you are unable to make payments on time and you owe more than your assets are worth.

The amount of time that a bankruptcy filing takes depends on how many times you have filed for bankruptcy in Canada and whether or not you will be required to make surplus income payments.

When you have your first bankruptcy, you can receive a discharge in as few as nine months. This is subject to change depending on your income. If you are required to make surplus income payments, the time for a first bankruptcy will be extended to 21 months.

If you need to declare bankruptcy a second time, it will take much longer. A second bankruptcy will take a minimum of 24 months. This period increases to as much as 36 months if there is surplus income involved.

It’s rare, but some people have a third bankruptcy. If that happens to you, you’ll have to attend a discharge hearing in a bankruptcy court and explain to a judge why you had to file three times. This is something you clearly do not want.

It takes nine months for an “Absolute” discharge. The conditions for an “Absolute” discharge include:

- You must be in your first bankruptcy

You must have attended two counselling sessions

No income portion payments are needed

The discharge is not opposed by any creditor

If it’s a second bankruptcy, the time for eligibility for an absolute discharge is 24 months as long as no surplus income payment requirements or creditor challenges. Having surplus income will typically increase the time to up to 36 months.

Yes. A discharge might be opposed by creditors, especially if the person in bankruptcy failed to meet any obligations. The court will review the case and may not grant a discharge.

Declaring bankruptcy in Canada isn’t cheap. But the investment may well be worth it, depending upon your situation. The basic minimum cost for first time filers is $1,800. This cost – which can be paid in installments – covers administration fees, government fees, fees to your Licensed Insolvency Trustee, and other costs. This is known as the base cost.

Additionally, there can be two additional costs that you must cover depending on your situation:

1. Surplus Income: If your income is above a certain threshold, then you must make extra surplus income payments to your creditors.

2. Asset sale or equity costs: If you have assets that do not qualify for exemption in your province or territory, those assets may be sold to repay your creditors or you may need to pay costs if the equity of the assets is above a certain value.

There’s no way around it, declaring Bankruptcy is hard on credit. While in the process of bankruptcy, your credit score will be severely damaged. The bankruptcy will stay on your credit report for six years for a first-time filing and fourteen years for a second filing. All debts discharged through bankruptcy will be noted with an R9 (revolving) or I9 (installment) status. This will likely put you in the lowest tier of creditworthiness. However, with a clean slate after bankruptcy you can begin the process to rebuild your credit.

On a national level, most of your assets are NOT exempt from being discharged. There are, however, some exemptions for assets, including your Registered Retirement Savings Plan, except contributions from the previous 12 months. Personal clothing, pets, and low equity in assets such as a house (under $10,000) are exempted as well. Additionally, tools needed to work, some farm property, and household furniture in the home in which you permanently live are also exempt.

Provinces and territories also designate assets that qualify for exemption for residents who file for bankruptcy. Your trustee will be able to explain the exemptions where you live in detail, so be sure to ask during your consultation.

Bankruptcy does not eliminate all types of debt. Obligations such as child support, alimony, student loans that are less than seven years old, car loans (unless you give up the car), and your mortgage will remain. Taxes are not covered, and other legal fees involved in the process are not covered. Any debt due to fraud will also not be discharged.

Be aware that when you file for bankruptcy your records are kept by the Office of the Superintendent of Bankruptcy Canada (OSB). This means your filing is public record and anyone can look it up. The OSB also gives this information to the credit reporting agencies (credit bureaus).

Your bankruptcy isn’t published anywhere and while it is public record, the Canadian Government does not push this information out to anyone except creditors, credit bureaus, and your trustee.

It’s unlikely but possible someone could look up your bankruptcy. Also, when you apply for new credit, the potential new creditor will learn about your bankruptcy status.

Talk to a trained credit counsellor today to better understand your options for debt relief before you decide.