How to Reduce Credit Card Debt

Two proven methods of reducing high amounts of credit card debt that can save you time and money.

When you need to take down credit card debt, there are two basic ways to do it effectively. The method you choose depends on your unique financial situation and goals. Each method prioritizes your credit cards to create a repayment plan that lets you reduce debt as efficiently as possible.

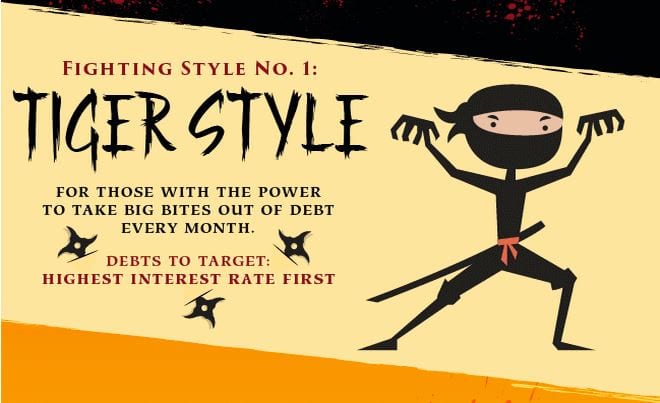

Tiger style debt reduction: High APR first

This is how to reduce debt fast so you can minimize interest charges. High APR debts eat up each payment, so eliminating them first reduces your total cost. The more money you have to make large payments, the faster this will go.

Here’s how to reduce credit card debt with this method:

- Use a credit card debt worksheet to list out all your debts. You specifically need to note each current balance and the APR.

- Prioritize the list from high interest rate to lowest.

- Now review your budget to cut any unnecessary expenses; this maximizes the cash flow you have available to pay off debt.

- Make the minimum payments on all your debts except the one with the highest interest rate.

- Then make the biggest payment possible on the debt with the highest APR.

- Keep that up until the debt is gone, and then move on to your next highest APR debt.

- As you eliminate each debt, you free up more money to pay off the next. This accelerates repayment until you reach zero on all your balances.

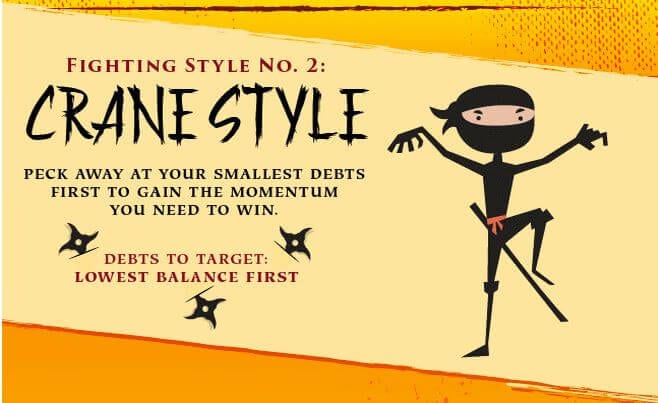

Crane style debt reduction: Low balances first

If your highest APR debts are also your biggest balances, tiger style may not work effectively. Basically, you may not have enough power to tackle your largest debts first. In this case, you organize your debts starting with the lowest balance.

All the steps listed above are the same. However, you pay off the lowest balance first. This frees up money to pay off your next smallest balance.

Each small balance eliminated gives you more cash to pay off the next. This way, you accelerate faster to more cash freed up.

With crane-style you essentially start pecking away at your debts. Each debt repayment you knock down gives you more pecking power to take out the next. By the time you get to your biggest balances, such as a student loan, you have the cash flow you need to take them down.

Comparing do-it-yourself debt reduction to other options for relief

It’s important to recognize that a do-it-yourself debt reduction strategy may not always be the best solutions for debt problems. There are debt relief alternatives that may allow you to:

- Get out of debt faster to save time

- Minimize total interest charges to save money

- Reduce the monthly payments to save you from juggling bills

Different debt solutions offer different benefits, so it’s important to compare your plan to reduce debt to these other solutions. There are three basic solutions you can use for debt relief that won’t damage your credit score or increase financial risk:

- Credit card balance transfer

- Personal debt consolidation loan

- Debt management program

Other options exist, but they either damage your credit or increase your risk, like debt settlement. For example, you can use a home equity loan to pay off credit card debt. However, this means you can be at risk of foreclosure if you default. That’s why we don’t consider this option when comparing good solutions to get out of debt.

I lead one of Canada’s largest credit counselling non-profits and we’ve helped hundreds of thousands of people pay off their credit cards. But some Canadians want to do it on their own, and I applaud them for that.

If you’re one of those DIY people, let’s talk about two tactics you can take by yourself. First, there’s a personal loan. That’s right, you’re taking out a loan to pay off your credit cards.

The thing is, a personal loan’s interest rate is much lower than the sky high rates on your credit cards. So while you’re still paying off a loan, you’re actually saving money. You’re also paying off one loan instead of trying to juggle a bunch of credit card statements. Forget to pay one of them and you face steep finance charges.

The other tactic has a long name but a simple concept: introductory 0% balance transfer cards. These are credit cards that feed on other credit cards. They want you to transfer all your credit card balances to their card and while they often charge you a small fee to do so, they lure you in with an amazing offer. Pay no interest for 6, 12 or even 18 months.

What’s the catch? Simple. Once that introductory period expires, you pay full interest once again. So if you can pay off your balance within those few 0 interest months, you save big. But if you don’t, well you might actually pay even more interest than you did before. Even if you want to do it yourself, I urge you to call consolidated credit for a free debt analysis from one of our trained counsellors.

It’ll help you figure out all your options, whether its DIY or with expert assistance, then you can choose. The call is free and unlike those 0% introductory offers, our help never expires.

Featured Video:

How to Pay Down Credit Card Debt on Your Own

Executive Director of Consolidated Credit Jeff Schwartz discusses some simple steps you can do on your own to bring down your credit card debt over time.

The secret to reducing debt faster

If you wonder why you can’t make any headway in reducing debt, look no further than your credit card APR. High interest charges eat up the majority of every payment you make, making it impossible to reach zero. Learn how to find debt solutions that reduce or eliminate interest charges so you can reduce credit card debt fast and regain stability.

Reducing debt with lower payments

When you can’t afford to make ends meet with your current payments, there are ways to eliminate debt for less. These solutions focus on adjusting the interest rate applied to your debt, so you can reduce it efficiently. Then you pair this with a repayment plan you can afford on your budget. As a result, you can get out of debt faster even though you pay less each month.

How long should debt reduction take?

A debt reduction plan is only as good as your ability to execute it successfully. Plans that take too long usually lead to even more problems with debt. This page teaches you how to set reasonable expectations on how long it takes to reduce credit card debt. Armed with this knowledge, you can compare debt relief options to find the best solution for your needs.

Ready to achieve debt freedom? Contact us today to speak to a trained credit counsellor.