Consumer protection laws aim to safeguard fair trade, prevent fraud, and protect consumer rights. In Canada, it’s the Financial Consumer Agency of Canada (FCAC), along with some provincial/territory laws, that uphold these safeguards. These rights include the right to information, safety, and voicing complaints.

With the use of consumer protection laws, we’ll explore how you can protect yourself from credit card scams. You’ll find out who to reach out to if you’re ever targeted by a scammer, and your rights and responsibilities regarding your credit card.

Consumer protection laws when dealing with financial institutions

Your rights when opening up a credit card

Understanding your rights is important when you get a credit card. It aids in recognizing your obligations, as well as, those required to be upheld by credit card issuers. Being informed of these rights and obligations will protect you should your rights ever be violated.

Some of the key rights to know:

- If your credit card company changes any features of your credit card, they must provide you with written details 30 days before the changes are implemented.

- Accessing key information like interest rates, fees, and additional charges is a right granted to you when applying for a credit card.

- Before increasing your credit card limit your credit card company has to get your permission.

- Each billing period, your credit card issuer is obligated to send you a statement that lists your annual interest rate, current balance, minimum payment, and the due date. This statement can be sent through mail or email.

Your rights regarding credit card balance insurance

Credit card protection is in place to help debtors protect themselves financially. Balance insurance protects you when you are having trouble paying for your credit card. If you can’t pay your credit card bill on time, balance insurance coverage can keep your account in good shape. However, balance protection is only available for dire situations like unemployment, sickness, or death.

Credit card companies must get your consent to put this protection option on your account. They aren’t allowed to violate your rights by adding it in as part of their service and not telling you. Leaving you with an unexpected expense like Kris Holmberg.

CBC News shared Kris’ story. They explained that for 10 years he was unknowingly paying balance insurance. All said and done he had paid out $9,090 for coverage he didn’t need as he was already protected by life insurance. Holmberg reached out to his bank. He asked for proof of the transaction, such as a voice recording or an email showing he signed up for the insurance. The bank couldn’t provide any evidence that Holmberg authorized the insurance. As a result, they had to refund him his money back.

What are your rights when using credit card cheques?

The unfortunate thing about credit card cheques is that banks aren’t exactly forthcoming about the financial impact they have. With how well they pad their bottom line it’s to their advantage not to share that information. The main benefit being that these cheques are treated similarly to cash advances. Making them one of the most expensive forms of credit on the market. Luckily, there are now policies in place to protect consumers. Here are some of them:

- If you verbally approve of receiving cheques, your bank, or credit card issuer, must provide you with written confirmation of it. You must receive this document by the date of the first credit card statement provided after your consent.

- Using a credit card or other services from a financial institution does not imply your authorization for them to send you credit card cheques.

How are you protected against unauthorized credit card transactions?

If your credit card is stolen, you won’t have to worry. The FCAC consumer protection laws state that credit card companies must guarantee customer protection. Thus, if someone steals your card, you may only be held liable for up to $50. However, you won’t be responsible for any major charges you didn’t make.

When your credit card is stolen, here are some things that you can do:

- Call your credit card company and report your card as stolen.

- Cancel your credit card.

- Keep an eye on your credit report for things such as, fraudulent credit being opened in your name.

- Review your account for any abnormal transactions and record them.

- File a police report.

Consumer protection laws against fraud

It’s tempting to think fraud can’t happen to you, but it can. There are multiple ways for fraudsters to get ahold of your information. They can steal your wallet or purse. Go through your mail or garbage searching for your credit card or bank statements. They can also hack your computer and get your bank account number, online banking password, and credit card information.

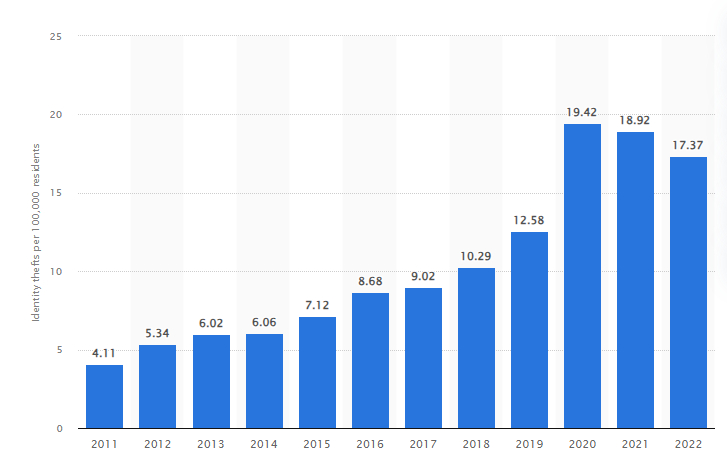

According to data by Statista, every year thousands of Canadians have their identities stolen. In fact, as their chart below states, from 2011 to 2020 the number of Canadians who had their identities stolen was on the rise.

While the number of cases has dropped slightly since then, it’s still much higher than before. With technological advances continuing to make leaps and bounds, there’s an argument for the idea that numbers will, at the very least, stay the same if not go up again. Credit cards are a particularly common avenue for identity theft.

Common forms of ill intent involving credit cards

Subscription traps

Many respectable companies offer monthly subscriptions for their products and services. Unfortunately, some not-so-respectable companies also use subscription models in sneaky ways to grab ahold of the hard-earned money of Canadians.

For example, some companies don’t mention anything about a subscription until you reach their product checkout page. Even then, it’s often in small print with a small checkbox that you have to click to opt out of the subscription. By making the subscription a discreet opt-out, instead of an opt-in, option it makes it easy for customers to miss. Leaving them surprised and confused when they see the subscription pop up on their credit card statement.

Here is how you can protect yourself from subscription traps:

- If a product or service offer appears too good to be true, and you sense something is off, research the company and read its customer reviews.

- Check your credit card statement regularly for unknown or unexpected charges.

- If a business has lured you into a subscription trap, contact your credit card issuer. They may be able to refund the subscription fee.

Spam

Spam is a common method hackers use to access your credit card information and other data stored on your PC. It can come in the form of unwelcome emails, unsolicited software, text messages, and phone applications. It’s important to be vigilant about what communications you interact with.

Fortunately, there are now consumer protection laws in place to help protect Canadians by minimizing malicious intent communications. It’s called the Canadian Anti-Spam Law (CASL) and came into effect on July 1st, 2014. According to the law, any business that is going to send commercial electronic messages by email must agree to the terms and regulations of the CASL. If an organization violates these regulations, it can face up to 10 million dollars per violation.

The CASL defines spam as:

- Unauthorized alteration of transmitted data

- The installation of computer programs without consent

- False or misleading electronic representations (including websites)

- The harvesting of addresses (collecting and/or using email or other electronic addresses without permission)

Here are some of the regulations in effect:

- Enterprises cannot send marketing emails without the person’s permission.

- Organizations may not represent themselves falsely

- Email addresses cannot be gathered without permission

- Companies can’t gather personal information illegally by accessing computer systems or electronic devices

Spyware

Spyware is malicious software. Having spyware on your computer can slow it down and make it susceptible to cyber-attacks.

You can find free applications that contain spyware on plenty of web pages. Spyware is defined as applications that download and monitor your data without consent for commercial purposes.

Spyware grants digital criminals access to your computer and its information. This involves private information, such as your credit card numbers, bank account numbers, and online passwords. With this information, hackers can steal money from your account and buy items online with your credit card information.

Here is how to protect yourself from spyware:

- If you’re unfamiliar with the website you’re on, and they ask you to download a program, check its reviews. Also, it’s a good idea to research more information about the program.

- Protect your data by downloading a trusted and well-reviewed antivirus program.

- Ensure your computer settings are set to “ask for permission” before software updates. This stops spyware programs from updating on your PC.

Steps for safeguarding yourself against fraud

Don’t share your credit card

If you have doubts about sharing your credit card, avoid it. Also, remove your credit card details from any computer or device that isn’t yours. This includes phones and tablets. It’s even better to avoid using your card on devices you don’t own.

Stay vigilant

Keep track of your credit card statements and bank account and watch out for suspicious activity. Shred all your paper bills and bank statements before throwing them in the garbage.

Avoid using public Wi-Fi

To prevent your private information from being stolen avoid using public Wi-Fi. This means you shouldn’t use Wi-Fi in places like the library, coffee shop, the gym, and even at a movie theatre.

Get reliable antivirus protection

Use reliable antivirus software to keep your identity and credit card information safe. This helps stop cyber hackers from getting into your computer and stealing sensitive information.

What can you do when you have been scammed?

Getting scammed is awful. However, it isn’t the end of your financial future. There are things you can do to recover your confidence if it has happened to you.

Relax

Being the victim of a scam can be extremely stressful, but it’s important not to panic. Take a moment to unwind and carefully evaluate the situation.

Gather important documents

Gather any documents containing evidence of where the company or person who has scammed you is located. You also should look for documents that state when, where, and how they have contacted you.

Contact your bank

Get in touch with your financial institutions and inform them that someone has scammed you. Bank employees will be notified to monitor any unusual transactions that occur on your accounts.

Report the scam

You should report the scam to the Canadian Anti-Fraud Centre (CFAC). They are Canada’s national organization that enforces the laws involving fraud.

Monitor your credit report

If you encounter a scam, it’s a good idea to monitor your credit report. This will help you detect any identity theft or suspicious activity. Additionally, you can set up an alert on your credit report to receive notifications if anything unusual appears.

Final Thoughts

The Chartered Professional Accountants of Canada commissioned market research company Ipsos to conduct a survey about fraudulent activity in Canada. The results revealed that almost half of Canadians have been victims of fraud or scams. There’s no easy way to stop this from happening. That’s why it’s important to contact the FCAC If you believe an organization has violated consumer protection laws. They can assist you in navigating the issue. You’ll also be helping them. They use the details from all cases they hear about to help create a plan of action to stop these situations from happening.

Key Takeaways

- There are numerous consumer protection laws that protect Canadians, including those that have a particular focus on credit cards.

- The Canadian Anti-Fraud Centre is the regulating and enforcer of these laws. Contact them when you feel that your rights have been violated.

- There are simple things you can do to protect yourself from your credit card information from being stolen such as shredding documents, reading agreement terms, and installing anti-virus software on your computer.

FAQ

Who regulates credit card companies in Canada?

The Financial Consumer Agency of Canada regulates how credit card providers should conduct themselves. It sets the rules for their services.

Is it illegal to have someone’s credit card info with no intention of using it?

It is illegal to hold someone else’s credit card information without their consent. This action can lead to legal consequences.

Is it against the law for a company to keep your credit card on file?

No, it is not against the law for a legitimate organization to keep your credit card on file.