Buying a Home

The home buying process can be very intimidating especially if you don’t know where to start. This educational booklet is a combination of information from Consolidated Credit Canada and the government of Canada to get you started on the road to making one of the biggest and most important purchases of your life.

Congratulations on taking this important step to a brighter financial future. Consolidated Credit Canada has been helping Canadians across the country solve their credit and debt problems for years.

Our Educational Team has created over twenty-five publications to help you improve your personal finances. By logging onto www.consolidatedcreditcanada.ca you can access all of our publications free of charge. We have tools to help you become debt-free, use your money wisely, plan for the future, and build wealth. The topics Consolidated Credit Canada addresses range from identity theft to building a better credit rating; from how to buy a home to paying for university. On our website, you will also find interactive tools that allow you to calculate your debt and see how much it is costing you.

We are dedicated to personal financial literacy and providing a debt-free life for Canadians. If you are overburdened by high-interest rate credit card debt, then I invite you to speak with one of our trained counsellors free of charge by calling (844)-402-3073 for free professional advice.

Sincerely,

Jeffrey Schwartz

Executive Director

Consolidated Credit Canada.

Home Buying

Can I Buy a Home?

The home buying process can be very intimidating especially if you don’t know where to start. This educational booklet is a combination of information from Consolidated Credit and the government of Canada to get you started on the road to making one of the biggest and most important purchases of your life.

The first question you are probably asking yourself is whether or not you can afford to buy a home. If you can afford it, what price range should you be looking at and will you qualify for the loan? There are a couple of things that you should look at when you find yourself asking these questions.

First, you need to know what your income and current expenses are. The Canadian government recommends that your mortgage payment should not exceed 30% of your income. Keep in mind that your mortgage payment is not going to be your only additional expense when buying a home.

How Much Do You Really Earn?

Before you can figure out your housing and debt ratios, you must be clear about how much you earn, in terms of your gross monthly income. Gross monthly income is your income before taxes. If you are paid an annual salary then take that salary before taxes or retirement plans are taken out. Divide it by 12, and that will give you your monthly income.

If you are paid hourly or weekly, take your hourly pay and multiply it by the number of base (or regular) hours you work each week. Then multiply that by 52 (the number of weeks in a year) to give you an annual number. Divide that by twelve (the number of months in a year) to get your monthly income.

Let’s say you earn $20/hour and you normally work 25 hours a week. You’ll take 20 and multiply it by 25 = 500 to get a weekly figure. You’ll then multiply 500 x 52 = 26,000 to get an annual figure. Then divide 26,000 by twelve to get a monthly income of $2166.

In calculating your income, a lender must allow you to include:

• Child support or alimony, usually if it will continue for at least another 3-5 years.

• Retirement income, including CPP benefits or a company-provided pension as long as it will continue.

If you have income from a side business or if you are self-employed, you’ll need a lender that has programs for the self-employed. If you receive overtime or bonuses, the lender will generally need to document that pay is regular and likely to continue.

Your annual income $_______________

Divide that by 12 ÷12_____________

Equals your gross monthly income $_______________

If you are paid hourly

Your hourly pay $_______________

Multiply by the number

Of base (or regular) hours you

Work each week x________________

Multiply by 52 (weeks in a year) x52 ______________

Divide that by 12 ÷12_____________

Housing Ratio

Now that you have your monthly income, you can calculate your housing ratio. The housing ratio is the amount of your monthly income that goes to pay your housing payment. A housing ratio of 28% or less is considered ideal. Multiply your monthly income by .28 (or 28%). That’s the maximum amount a lender would generally say should go toward your total monthly housing expense.

In our example above, the lender would want to see a total monthly payment of no more than $606.48. ($2166 in monthly income x .28 = $606.48)

Keep in mind that monthly housing expense doesn’t just include the loan payment. It should also include taxes and insurance, and condo fees if there are any. You can ask a real estate agent to estimate those costs for you in your price range.

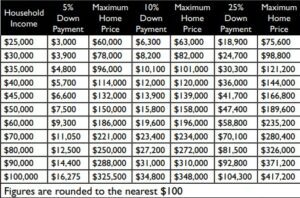

To get more information on what you can afford and access several calculators go to www.cmhc-schl.gc.ca. Here you will find the website for the Canada Mortgage and Housing Corporation.

This table assumes a mortgage interest rate of 8%, average tax and heating costs in Canada, and the mortgage an average Canadian would qualify for based on a 32% debt service ratio (Source CMHC).

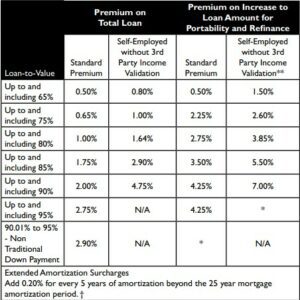

Below is a table with information regarding mortgage insurance. If you are unable to put 20% of your purchase price down on your home, you may be required to pay mortgage insurance. With mortgage insurance, you are able to put down as little as 5%. CMHC is one of the primary providers of this insurance and their premiums are as follows (Source CMHC):

How Much will it Really Cost? (This information is provided by the Canada Mortgage and Housing Corporation)

Once you have figured out the home price range you can afford and the type of mortgage you qualify for, you will need to calculate all of the associated costs of the transaction to make sure you are financially ready.

Up-Front Costs

You will need to plan ahead to cover the many up-front costs of buying a home. Timing is important to help make sure things go smoothly.

Mortgage Loan Insurance Premium. If yours is a high ratio mortgage (less than 20% down payment), you may need mortgage loan insurance. To get this insurance, you will be asked to pay the required insurance premium. Your lender may add the mortgage insurance premium to your mortgage or ask you to pay it in full upon closing.

Appraisal Fee. Your mortgage lender may require that the property be appraised at your expense. An appraisal is an estimate of the value of the home. The cost is usually between $250 and $350 and must be paid when you contract for those services.

Deposit. This is part of your down payment and must be paid when you make an Offer to Purchase. The cost varies depending on the area, but it may be up to 5% of the purchase price. If you wish to make a down payment of 5% and you give a deposit of 5%, then your down payment is considered to be made.

Down Payment. At least 10% of the purchase price is usually required for a high-ratio mortgage and at least 20% of the purchase price is usually required for a conventional mortgage.

Estoppel Certificate Fee (not applicable in Quebec). This applies if you are buying a condominium or strata unit and could cost up to $100.

Home Inspection Fee. Remember that this may be a condition of your Offer to Purchase. A home inspection is a report on the condition of the home and may cost over $200, depending on the complexities of the inspection. For example, it may be more costly to inspect a home that has large square footage, one that is expensive or one where contaminants such as pyrite, radon gas or urea-formaldehyde are suspected.

Land Registration Fees (sometimes called a Land Transfer Tax, Deed Registration Fee, Tariff or Property Purchases Tax). You may have to pay this provincial or municipal charge upon closing in some provinces. The cost is a percentage of the property’s purchase price and may vary. Check with your lawyer/notary to see what the current rates are.

Prepaid Property Taxes and/or Utility Bills. To reimburse the vendor for pre-paid costs such as property taxes, filling the oil tank, etc.

Property Insurance. The mortgage lender requires this because the home is security for the mortgage. This insurance covers the cost of replacing the structure of your home and its contents. Property insurance must be in place on closing day.

Survey or Certificate of Location Cost. The mortgage lender may ask for an up-to-date survey or certificate of location prior to finalizing the mortgage loan. If the seller does not have one or does not agree to get one, you will have to pay for it yourself. It can cost in the $1,000 to $2,000 range.

Water Quality Inspection. If the home has a well, you will want to have the quality of the water tested to ensure that the water supply is adequate and the water is potable. You can negotiate these costs with the vendor and list them in your Offer to Purchase.

Legal Fees and Disbursements. Must be paid upon closing and typically cost a minimum of $500 (plus GST/HST). Your lawyer/notary will also bill you direct costs to check on the legal status of your property.

Title Insurance. Your lender or lawyer/notary may suggest title insurance to cover the loss caused by defects of title to the property. If you feel you cannot cover all of the up-front costs, you can ask your lender for a loan. Remember that payment for this loan amount, based on a 12-month repayment period, will have to be included in your Total Debt Service ratio calculation.

Other Costs

Besides up-front costs, there are other expenses to consider:

1. Appliances. Check to see what comes with the house, if anything.

2. Gardening equipment.

3. Snow-clearing equipment.

4. Window treatments. Check to see what comes with the house.

5. Decorating materials. Paint, wallpaper, flooring and tools for redecorating.

6. Hand tools. You will need some basic hand tools for your new home.

7. Dehumidifier. May be required to control moisture levels, especially in older homes.

8. Moving Expenses.

9. Renovations or Repairs.

10. Service Hook-Up Fees. Charged for utilities. You may be required to pay a deposit for utilities such as telephone and heating services.

11. Condominium Fees. You may have to make the initial payment for these monthly fees.

While You’re Spending all of this Money, Why Not Save a Little?

There are many ways to cut the expenses of home buying as well. From buying to remodelling, to repairs, being a sensible consumer pays.

Buying a home, as you can imagine, is expensive. As with any financial venture, education is the key. Before you consider starting the house-hunting process, be sure to sit down and review your financial situation thoroughly. While owning will result in equity and money well-spent, you need to make sure you have the money first. It is always a good idea to sit down with a trusted financial planner as well so you have a second pair of eyes looking at your situation.

After you have made the leap into homeownership, you will have many new responsibilities that you should consider.

Home Repairs

Home repairs are unavoidable even if you build a brand new home. Ensure that you understand your home warranty when you are purchasing and building your home. With a new home, many builders ask that you keep a list of anything that goes wrong with the house with the promise that they will return to fix issues within the first year. They WILL NOT come knocking on your door offering to fix anything that may be wrong. Make sure that you keep a thorough list of problems like nail pops, cracks, leaks, etc. Use tape to mark anything that you may forget the location of later. Contact your builder periodically to let them know that you are expecting them to follow through on their promise. They already have your money so make sure you continue to motivate them. You are the customer.

Decorating

Although this is one of the most fun parts of owning a new home, it can also be the most expensive! There are, however, many ways to decorate on a sensible budget and still have a great-looking home! Painting is one of the most inexpensive ways to make your house look beautiful. It is a great way to put your personal touch in each room without spending a fortune. Buy your paint at a home-improvement store like Rona or Home Depot and don’t be fooled by name-brand paint. The store brands usually have a wide variety of colours and look just as great on your walls. Sticking with neutral colours may be your best bet if you are someone who often likes to change the look of a room. With neutral walls, you can change the lighting or the accessories in a room when you are looking for an update. Updating furniture can be costly as well, so take the time to look into slipcovers or re-upholstering furniture yourself. A great rule of thumb is to stick with neutral when you are spending a lot (like furniture) and go bold when you are spending a little (like vases or candles). Again, home improvement stores offer books with clear and easy instructions on many do-it-yourself projects. Replacing throw pillows can also add a lot to a room without spending the money on new furniture. Yard sales and flea markets are also great ways to find unique ways to decorate. It can be a lot of fun negotiating too! Never pay full price for something second-hand. Another great way to decorate is with photographs. Traditional framed pictures of family are beautiful. If you are more of a non-traditional person, take pictures of abstract things and use websites like www.shutterfly.com or www.kodak.com to enlarge and edit pictures to get even more creative. Look for frames on sale at discount stores and make your home into a story!

Heating and Cooling

One of the best-proven ways to cut down on heating and cooling costs is to purchase and install a programmable thermostat. This allows you to adjust the temperature of your home automatically throughout the day. Many homeowners program the house to be cooler an hour after going to bed and to start heating up again an hour before they wake up. Also if you are at work during the day, it’s a good idea to keep your home cooler in the winter and warmer in the summer while you are away. Programmable thermostats can be found at stores like Rona and The Home Depot and are fairly simple to install.

Simple things like using blankets and slippers in the winter can also save money on heating your home. Lower your thermostat by a couple of degrees and snuggle up on the couch!

Electric

Make sure you turn your lights off as well. Make it a habit of turning lights off when you leave a room and try not to use accent lighting. It may look pretty but the cost is not worth it. If you enjoy decorating during the holidays, invest in LED lights. They use significantly less energy and they still look beautiful. Be sure to put your holiday lights on timers as well since they can’t be seen during the day anyway!

Phone

Everyone carries a cell phone now, so make sure you are not spending a fortune on both your home phone and your cell phone. If you are an avid cell phone user, make sure that you have a plan that suits you. It doesn’t make sense to have unlimited text messaging if you don’t use the option on your phone. Also, call your residential phone company and find out what the most inexpensive service package is. This way, you are only paying for options on one phone instead of both. If you are not much of a cell phone user, cut back on what you are spending on your mobile plan.

Cable/Satellite

It is very tempting to have premium channels and sports packages included with your cable service, but it comes with a price tag. Before you commit to paying more for premium channels, make sure you really monitor how much you are watching them. Call your cable company and see if they have any free trials available. If so, record how much time you spend watching each premium channel during the trial period and decide whether you watch them enough to make it worth the price.

Homeownership is something to really be proud of. Being a smart homeowner comes with experience and education. Make sure you take advantage of all of your resources as a homeowner so you are enjoying your investment while maintaining it wisely!

The following websites are fantastic resources for homeowners:

Canada Mortgage and Housing Corporation

http://www.cmhc-schl.gc.ca/en/co/buho/

Canadian Consumer Information Gateway

http://www.consumerinformation.ca

Canadian Home Builders’ Association

http://www.chba.ca/

About Consolidated Credit Canada

Consolidated Credit Canada is a consumer-oriented, non-profit organization. We are an industry leader in providing credit counselling and debt management services. Our mission is to assist individuals and families in ending financial crises and to help them solve money management problems through education, motivation, and professional counselling. Our organization is funded primarily through voluntary contributions from participating creditors. Our programs are designed to save our clients money and liquidate debts at an excellent rate.

We are dedicated to empowering consumers through educational programs that will influence them to refrain from overspending and abusing credit cards, as well as to encourage them to save and invest. Regardless of whether your financial problems are due to the purchase of a new home, the birth of a child, major illness, or any other circumstance, we can help.

* If you are headed for a debt disaster visit www.ConsolidatedCreditCanada.ca or call (844)-402-3073 for free professional advice by a trained counsellor.