Budgeting Made Easy

This publication teaches how to successfully manage money and avoid credit problems. This guide provides money management techniques that can put readers in control of their money and help them plan for a successful financial future. We have created this guide with two purposes in mind; first, to help people create and use a successful budget; second, to provide proven strategies for avoiding excess debt.

Congratulations on taking this important step to a brighter financial future. Consolidated Credit Canada has been helping Canadians across the country solve their credit and debt problems for years.

Our Educational Team has created over twenty-five publications to help you improve your personal finances. By logging onto www.consolidatedcreditcanada.ca you can access all of our publications free of charge. We have tools to help you become debt-free, use your money wisely, plan for the future, and build wealth. The topics Consolidated Credit Canada addresses range from identity theft to building a better credit rating; from how to buy a home to paying for university. On our website, you will also find interactive tools that allow you to calculate your debt and see how much it is costing you.

We are dedicated to personal financial literacy and providing a debt-free life for Canadians. If you are overburdened by high-interest rate credit card debt, then I invite you to speak with one of our trained counsellors free of charge by calling (844)-402-3073 for free professional advice.

Sincerely,

Jeffrey Schwartz

Executive Director

Consolidated Credit Canada.

Budgeting Can Be Easy: What You

Need To Know

Learn how to successfully manage your money and avoid credit problems. This guide will give you money management techniques that can put you in control of your money and help you to plan for a successful financial future. We’ve created this guide with two purposes in mind:

• To help you create a successful budget and use it.

• To give you proven strategies for avoiding excessive debt.

Making the most of your money can be tough, but without a budget, it is nearly impossible.

Budgeting can be easy if you utilize the right tools and guidelines. Remember, now is a great time to learn how to create and live within a budget. The more you delay the budgeting process, the longer you will be in financial chaos. If you don’t learn to manage your money now, the headaches your debts create may stay with you for a long time.

At Consolidated Credit Canada, Inc. we help many individuals and families who are in debt. Our goal is to help you avoid problems and become financially successful.

Credit Card “Come-Ons”

“As a first-year student in University, different credit card companies that were soliciting their cards lured me in. At first, I figured one credit card was good enough for me. I did not have a real full-time job but I made a little money working as a tour guide.

The offers just kept coming in. Before I knew it I had at least 6 cards under my belt and a burden of debt on my shoulders. Now as a mother of a one-and-a-half-year-old, my student debt has affected me greatly.

I am unable to get a decent apartment or rent a house because of my credit and I am unable to get approved for loans. The harassment, threats of lawsuits, constant letters and bills really have taken a toll on my life. If I could change the past I would.

Currently, I still have the credit card debt I created when I was a student and it will take me years to pay it off because of my other obligations. I hope I can help someone else with my story because getting yourself into a whole lot of credit card debt is just not worth the headaches and rejection.”

Now she is a Consolidated Credit client and on her way to being debt-free.

Managing Debt

You can not achieve financial freedom without budgeting. Why? People who can account for their money are in control of it. You can not run a business successfully without a business plan. And you can not successfully run your household without a budget.

Start this process by writing down your fixed monthly expenses like rent, car payments, and insurance. Then make a list of your flexible expenses like groceries, hydro, gasoline, and incidentals. Finally, list discretionary expenses such as clothes, entertainment, etc. Make sure not to leave anything out; don’t forget your morning cup of coffee or your newspaper! The key is to include every expense from a Loonie to your mortgage payment. Review your bank statement or online Interac history to see where you’ve been spending money.

Use these suggested percentages for spending and see how your spending compares.

Housing 25%

Savings 15%

Transportation 15%

Utilities 10%

Food 10%

Clothing 5%

Medical/Health 5%

Personal 5%

Entertainment 5%

Debts 5%

Tips for Smart Credit Use

• Shop around for the best credit card interest rate. Consider using one card for balances that you will pay in full and another card with a low interest rate for times when you need to carry a balance. A list of credit cards is available at creditcardscanada.ca.

• Do not pay interest on items you don’t really need, or for things that will be gone by the time you get your bill. If you do, it’s like buying something for more than the ticket price.

• Read your credit card agreements and the correspondence you get from your creditors. There may be important information in them. For example, credit card issuers can generally change your interest rate with only 30 days’ written notice – even on a card with a fixed rate.

• Always mail your payments for your credit cards at least 7 business days before the due date or pay online when possible. Your interest rate on new purchases as well as any current balance may be raised to a very high rate if you are late. When you pay late, you become a risk to your bank. In order to mitigate that risk, your bank may raise interest rates or even close your account.

• Paying your accounts late can result in a rapid decline in your credit rating as well. Most creditors report payments later than 30 days to the credit bureaus and several, such as Sears, will report as soon as you miss your first payment. This history can stay on your credit report for up to ten years and it takes a lot longer to rebuild your credit history than it does to make it worse.

• Call your issuers if you are unable to make a monthly payment on time. Ask about alternative payment arrangements (payment holiday is one example) that won’t damage your credit or raise your interest rate. Do not wait until the due date arrives to call your creditors. Make sure that you call as soon as you become aware that you will not have the funds to pay.

• Notify your credit card issuer 30 days before you move, and do not assume that you do not have to pay the bill if you do not receive it. If a bill does not arrive, call your card issuer or lender immediately.

• Try to pay off your total balance each month. Paying the minimum payment is cheaper now but much more expensive in the long run. For example, if you pay minimum payments only on a $1,000 credit card balance with an 18% interest rate, it will take you more than 12 years to repay.

• Aim to keep your debt payments at less than 10% of your income after taxes. If you take home $750 a month, spend no more than $75 a month on credit.

• Be careful with financing that offers no interest, no payment for a specific period of time. Many furniture and electronic stores offer deals on a consistent basis. It sounds great when you are in the store; however, if you do not pay the balance in full by the date the promotion expires, you are billed for all of the interest that would have accumulated from the date of purchase. You are better off waiting to buy until you have saved enough money to purchase the item in full with cash or at least until you are able to put down at least 50% in cash.

The key to managing credit is not to get trapped in the mindset of “I’ll buy now and pay later.” When you do borrow, ask yourself how and when you will repay the debt and how much it will cost you. On the next page is a Borrowing Worksheet that we have created. Use this to keep track of

your debt and create a repayment schedule.

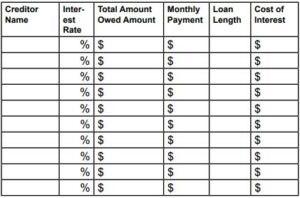

Borrowing Worksheet

On this worksheet, list your current loans or the loans that you are thinking about taking. Calculate the cost of the expected loan payments before you borrow and compare it to your income and outstanding obligations.

Average Interest Rate_____________________________

Total Amount Owed $_____________________________

Total of Monthly Payments $________________________

Total Time to Payoff ______________________________

Total Spent on Interest $___________________________

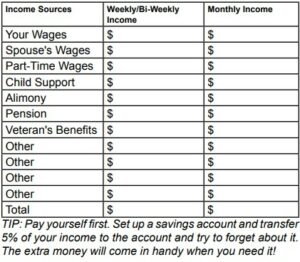

Income

The first step in creating your budget is to list all sources of monthly income, including gifts, bonuses, cost of living increases, allowances, etc. To total your income, use the following Income Worksheet:

Expenses

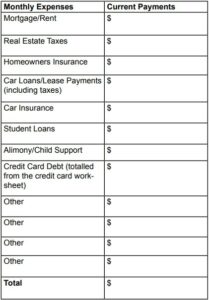

The next step is to list your expenses. Expenses are separated into three categories: “fixed”, “flexible”, and “discretionary.”

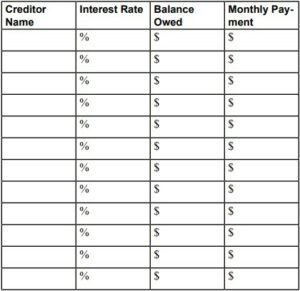

Credit Card Debt Worksheet

Credit card debt is considered a fixed expense because it usually remains the same each month. Use the following form to list your monthly credit card debt. List all major credit cards, department store credit cards, gas credit cards and dining cards. When you are finished, total the amount and transfer it to the appropriate column on the fixed expense worksheet on the next page.

Average Interest Rate of All Cards: _______%

Total Owed: $____________

Monthly Payment Total: $_____________

Fixed Expenses Worksheet

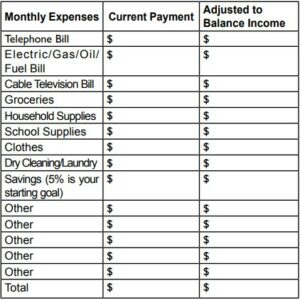

Flexible Expenses Worksheet

The next step is to list your Flexible Expenses. These expenses are ones where you control the amount of money you spend. Sometimes flexible expenses are items you need, like groceries, but you can control how much you spend on them by choosing less expensive items, shopping at discount stores, etc. Depending on your circumstances, a few of the items listed may fall into the Fixed Expenses category.

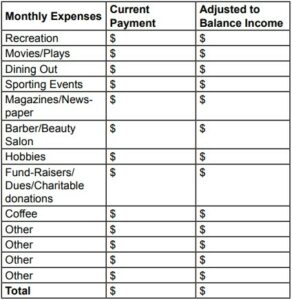

Discretionary Expenses Worksheet

The next step is to list all of the other expenses not listed in the previous categories. We call these Discretionary Expenses. These are items that are not necessary for survival. If your expense to income ratio is out of balance and you are spending more money than you earn, items from this category should be eliminated or cut back.

Where Do You Stand…?

Now that you have compiled your income and expenses, it is time to calculate the grand totals. All expenses are totalled and then subtracted from the total income figure for the month.

Next, divide total expenses by the frequency of income or the number of paycheques the household receives each month. This will tell you how much money to set aside from each paycheque. If the expense total is greater than the income total, you are off-track financially.

You must begin to prioritize expenses. Keep track of when you use credit cards. Then ask yourself if you want to borrow every month for these expenses. Each month, enough money should be set aside to cover fixed and some flexible expenses. This reserve method will save you from living paycheque to paycheque. Review the spending plan at the start of each income period. At the end of each month, compare actual expenses against what you budgeted. As time passes and you become adjusted to your budget, you may only need to perform this comparison quarterly.

End of the Month Budget Analyzer

After the second month of using your budget, utilize the following sheet to compare what you actually spent to the amount you budgeted. This will give you a clear picture of how realistic your budget is. This will also allow you to be more accurate when calculating your next monthly budget. Make enough copies so you can complete this exercise each month until the end of the year.

One Family’s Story

“We were the typical family living paycheque to paycheque with no savings and no money left well before the month ended. Paying bills was a nightmare, and going to the store was even worse. Money was in short supply and long on demand.

We used to go into a panic and blame each other if something unexpected happened, but now we have a little extra for those emergencies because we now know how to live on a budget.

With Consolidated Credit’s help, being able to pay all of our bills on time became a reality! Making a deposit into our savings account became a routine! The biggest thrill is seeing the credit card balances go down and knowing there is light at the end of the tunnel. Knowing that in a few years these huge debts that loomed over our heads as rain clouds would disperse and that we would be on our way to financial independence was wonderful.

However, the most important thing Consolidated Credit has given us is our self-respect and pride back. Life becomes less stressful and you can enjoy your children and participate in their lives instead of worrying about money and always telling them “No, we can’t afford it.” So, in essence, Consolidated

Credit’s Debt Management Program also allowed our kids to have happier childhood.”

Credit Tips To Live By

Always remember that credit is a loan. It is real money that you must repay.

Go slowly. Get one card with a low limit and use it responsibly before you even consider getting another.

Shop around for the best deal. Study your card agreement closely and always read the fine print inserts enclosed with every bill. Credit card offers vary substantially, and the issuer can change the terms with 30 days written notice.

Try to pay off your total balance each month. Paying the minimum can be very expensive.

Always pay on time. A single slip-up can place a negative mark on your credit report — and may cause your creditors to increase your interest rate to the maximum.

Set a budget, follow it faithfully and watch how much you owe on credit. A good rule of thumb is to keep your debt payments less than 15 percent of your net income after taxes.

Keep in touch with your issuer. In the event you must be late with a payment, call them before the due date. They may have alternate payment arrangements that won’t leave a negative mark on your credit rating. However, they may need some time to set up payment arrangements, so do not wait until the last minute to call.

At the first sign of credit danger, such as using one card to pay another, stop using the card, stop carrying it with you and only keep one card for emergencies.

About Consolidated Credit Canada

Consolidated Credit Canada is a consumer-oriented, non-profit organization. We are an industry leader in providing credit counselling and debt management services. Our mission is to assist individuals and families in ending financial crises and to help them solve money management problems through education, motivation, and professional counselling. Our organization is funded primarily through voluntary contributions from participating creditors. Our programs are designed to save our clients money and liquidate debts at an excellent rate.

We are dedicated to empowering consumers through educational programs that will influence them to refrain from overspending and abusing credit cards, as well as to encourage them to save and invest. Regardless of whether your financial problems are due to the purchase of a new home, the birth of a child, major illness, or any other circumstance, we can help.

* If you are headed for a debt disaster visit www.ConsolidatedCreditCanada.ca or call (844)-402-3073 for free professional advice by a trained counsellor.